My advice • December 18, 2019

modified on June 11, 2021

Budget planning interview: Getting a real picture of your finances

Interview with Michel Gariépy, an advisor at our Boucherville branch

Michel Gariépy

Michel GariépyAdvisor - Boucherville

- What advice would you give to clients that want to know more about their financial situation?

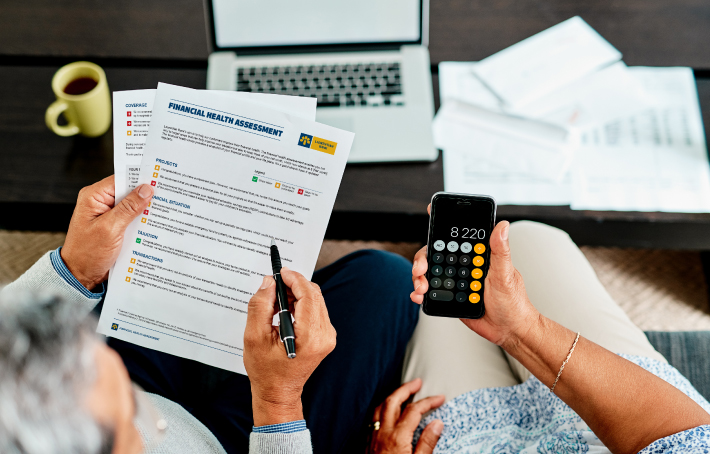

- It starts with a financial health assessment. This gives me an overview of my clients' goals, priorities, assets and liabilities, so I can provide them with the right advice. The first step is quite clear.

- What are the other steps toward better financial planning?

- You need to make a budget. This fairly simple exercise really pays off, because your personal finances will be better organized! I encourage my clients to use the budget tables on our website. Proceeding this way reduces the risk of missing things that might distort the overall picture. You need to include your income, like your salary or other revenue sources, and your expenses, such as your mortgage and other loans, outings and insurance. The key is to write down as much information as possible. You will know if your income covers your financial obligations and if you can save or not. We can then discuss your situation using actual data and create a budget plan that will help you better manage your personal finances. This budget will evolve based on your needs.

- What advice would you give to your clients to keep to their new budget?

- I recommend the weekly budget that we set in the first step using the table. This kind of budget quickly gives a good idea of any over-budget costs. All you have to do is check if you're on budget at the end of the week. If that's not the case, you can fix it by targeting your extra expenses. Going off budget once or twice isn't a big deal, but if it keeps happening, it's a sign that you need to reassess your situation and talk to an expert. It's highly recommended that you set aside part of your budget for savings. We call that “paying yourself first.” It's also wise to have a safety net in case of an unfortunate situation, like losing your job. Creating this financial cushion means saving the equivalent of three months' expenses. You will find this very helpful when the unexpected happens.

- Can you give us a few tips to avoid debt during the holiday spending season?

- I tell my clients to ask themselves the following questions before making a purchase: Is it an investment? Is it useful? And more importantly, do I need it? For major spending periods like the holiday season, I would recommend that you prepare a holiday budget in advance on what you plan to spend. Then you need to stick to it and don't go over, even if it's tempting!

- Any advice on getting out of debt?

- You need to take stock and pay your debts as quickly as possible. First, pay the debts with the highest rate and use the lowest-cost credit. You can sometimes use your mortgage, so you have to aim for as short an amortization as possible in order to reduce interests. An advisor is in the best position to help their clients in these types of situations.

- On the other hand, what you would say to clients with a surplus?

- Their entire financial situation needs to be reviewed. Is their credit report optimal, if applicable? Are there any loans they can accelerate payments on? Otherwise, they should set up an investment strategy using an Investment Plan with pre-authorized contributions (PAC). A set amount is withdrawn from your bank account and invested into mutual funds, based on your investor profile and at a frequency of your choosing, such as every two weeks, on pay day. The amount and frequency of your withdrawals can be changed at any time, based on your needs. This type of plan enables you to properly budget your surplus and make it grow as quickly as possible. Your advisor can help you choose an investment strategy. Ideally, you should meet annually to better assess your surplus and increase your PAC.

It's always a good time to plan. And it helps us get a better picture of your finances, so you can make informed decisions. Who doesn't want that?

+ Legal Notices

New investment accounts are offered by LBC Financial Services Inc. (LBCFS). Mutual funds are distributed by LBCFS. The Financial Planning service is offered by LBCFS. LBCFS is a wholly-owned subsidiary of Laurentian Bank and a legal entity distinct from Laurentian Bank and Mackenzie Investments. Mutual funds offered by LBCFS are part of the Laurentian Bank Group of Funds managed by Mackenzie Investments. A Laurentian Bank advisor is also a licensed LBCFS Mutual Fund Representative.

Commissions, trailing commissions, management fees and other expenses all may be associated with mutual fund investments. Nothing guarantees that the fund will maintain its net asset value per unit at a constant amount or that the full amount of your investment in the fund will be returned to you. Mutual fund values change frequently, and past performance may not be repeated. Please read the simplified prospectus or Fund Facts before investing in mutual funds.

The articles on this website are for information purposes only. They do not create any legal or contractual obligation for Laurentian Bank and its subsidiaries.

These articles do not constitute financial, accounting, legal or tax-related advice and should not be used for such purposes. Laurentian Bank and its subsidiaries may not be held liable for any damage you may incur as part of such use. Please contact your advisor or any other independent professionals, who will advise you as needed.

The articles may contain hyperlinks leading to external sites that are not managed by LBC. LBC cannot be held liable for the content of such external sites or the damage that may result from their use.

Prior written consent from the Laurentian Bank of Canada is required for any reproduction, retransmission, publication or other use, in whole or in part, of the contents of this site.